It seems hard to recall a world in which crowdfunding was not part of the financial lexicon, but in fact the industry’s mesmerising growth is a recent phenomenon.

Funding Circle dates from August 2010; Crowdcube got its FSA authorisation in the UK in February 2013. Even on the more traditionally institutional side, the straight-to-borrower private debt strategy of pioneering alternative asset manager BlueBay was only launched in 2011.

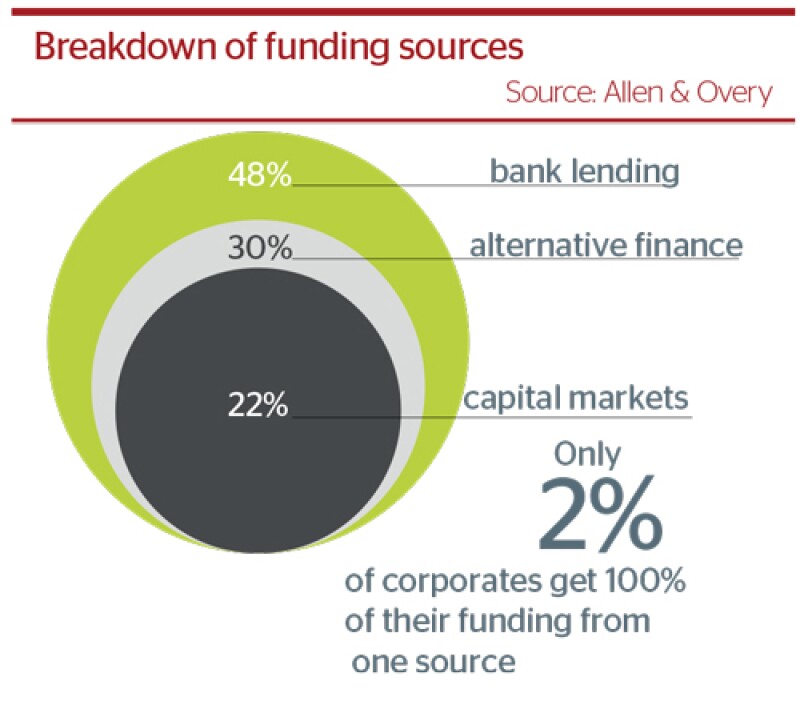

Yet it has transformed long-established models of financing, becoming part of the everyday furniture of capital raising with remarkable haste. According to a survey by Allen & Overy, the average composition of funding at medium to large non-financial corporates in western Europe is 48% bank lending, 22% capital markets — and 30% alternative finance.

Almost half of the corporates (48%) expect their use of alternative finance to increase over the next five years, more than any other market segment, while 57% of investors polled in the report say they expect to increase their provision of alternative finance. And that’s without looking at the small end of SMEs, who have benefited more than anyone from the arrival of these models.

Some natural questions arise, among them: how much share can these groups take? Is growth like this sustainable? What do the default rates look like? How much have they harmed the banks?

But perhaps the most striking question is: how on earth did a banking sector, starved of opportunities for growth in the post-financial crisis environment, allow a gap this big for a whole new industry to flourish within?

“Small businesses have been under-served by banks for decades, and the financial crisis only deepened the problem,” says Anil Stocker at MarketInvoice, a peer-to-peer lender whose model allows small businesses to sell their unpaid invoices to a pool of global investors, giving them swift liquidity and investors a strong return.

Damaged oligopoly

In the new world of banking, low-scale lending makes less sense, at least through traditional models. “In 2015 you still have to go to a branch and have an interview with an advisor to get a loan. It’s anachronistic,” Patel says. “And given banks’ cost of origination, with all these branches and advisers, they are migrating to larger loans of $2m-plus because of the hope that it will bring higher-fee ancillary services with it. That’s the only way a bank can justify dedicated relationship.”

That model, though, excludes the small borrower who has no major additional ancillary business to give. “And small businesses are the engine room of the economy: 60% of GDP in the UK,” says Patel. “They are underserved because banks can’t make it profitable.” It’s a problem that gets steadily worse with the capital requirements of Basel III. “From an ROE perspective and for bank shareholders, this is not as attractive to a bank as it used to be.”

That is the gap within which the crowdfunding industry has been able to establish itself and grow.

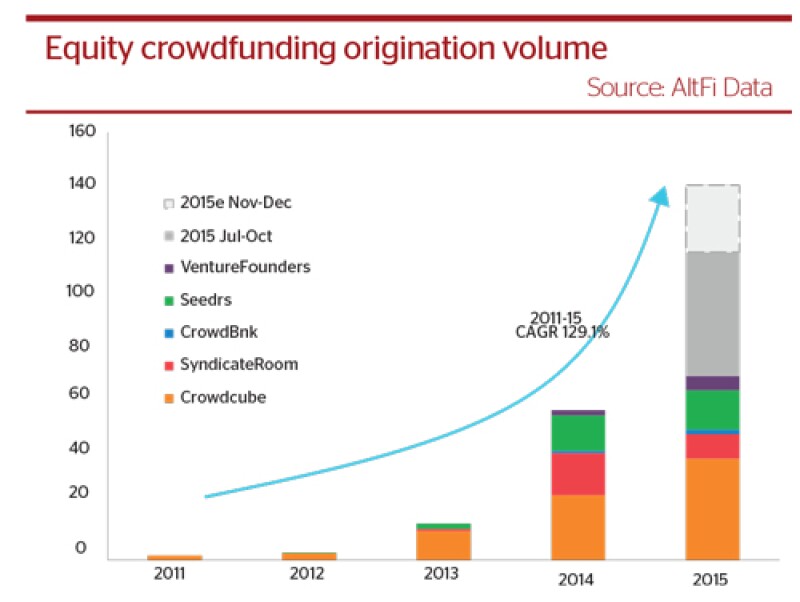

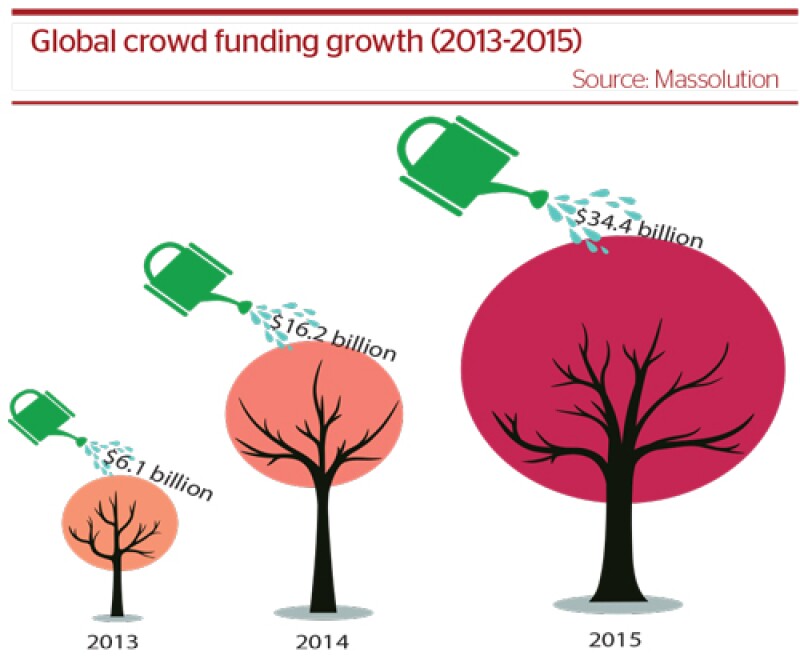

And then some. In July, the research group Massolution predicted the global crowdfunding industry would raise $34.4bn in 2015 — double the $16.2bn raised in 2014, which itself was well over double the $6.1bn total in 2013. To take the youngest company featured in this article, Crowdcube had by July 1 (when it was 29 months old as a licensed entity) put 231,172 investors together with 325 businesses in the UK, in one case raising the requested £1.2m for a business in just 16 minutes. Moreover, it’s a global phenomenon: while the US continues to dominate, accounting for $9.46bn and enjoying 145% year on year growth in 2014, it was in Asia that the fastest growth took place that year: 320% year on year, raising $3.4bn, according to Massolution.

Industrial evolution

At Crowdcube, for example, a vehicle called Mini-bonds was launched last year “as a way of enabling people to support and lend to more established businesses than start-up early stage equity investments,” says co-founder Luke Lang. The companies that back mini-bonds have typically been trading for 10 years or more and been profitable for some time. An example is the Eden Project, the environmental site in Cornwall; another is River Cottage, a UK cookery brand. At the time of writing, three Crowdcube companies were offering minibonds, each offering an 8% interest rate for terms of three to four years.

Crowdcube also offers the EIS Fund, which gives investors access to a diversified portfolio of underlying projects, suggesting the arrival of something of a mutual fund structure in the industry. “We recognise and understand investors are time-poor,” says Lang. “Many don’t have time to understand the business or don’t feel comfortable making investment decisions, so they place those decisions in the hands of a fund manager.” The manager in question is Crowdcube’s growth director Stuart Nicol, formerly investment director at Octopus Investments.

At Funding Circle, Patel’s very title — global co-head, capital markets — tells you something about the evolution of the P2P model. His job is to bring in institutional capital, and he says that’s a very interested constituency. “Very few new things have happened in the fixed income credit markets for a while,” he says. “Nothing exciting has happened in ABS-land since 2007-8, and what was exciting then was exciting for all the wrong reasons.”

The feedback he gets from investing institutions, he says, is that they are “finally able to access directly a new asset class”. The word directly is the point: this is not, strictly speaking, a brand new asset class, and Funding Circle keeps data going back to 1939 about the creditworthiness of new business, which in turn helps to give comfort to new institutional investors.

“Institutions are always a bit nervous when they see our tech engineers wandering around in flip-flops,” he says. “But when they do due diligence, they see that actually the loans are very traditional and that there is a huge amount of data available for them to back-test and portfolio-test.”

Additionally, although the average maturity of a Funding Circle loan is about 42 months, the levels of amortization prevalent in many of them means that the effective average duration is a shade below two years. “It’s a very short duration, high yielding fixed income asset, yielding just under 7%,” Patel says. “That’s impossible to find anywhere else.” It stands out particularly in an environment where interest rates are so low that most short-dated paper generates a negligible return.

Old and the new

Another sign of evolution is the way that other structures have fitted themselves to the broader P2P model. MarketInvoice is actually older than Crowdcube and Funding Circle, but its model represents a twist on the usual crowdfunding technique, albeit born out of the same post-crisis problems for small business.

“At the same time [as banks have withdrawn from small business lending] the lengthening payment terms of big business have created a perfect storm that the little guy struggles to ride out,” says Stocker. “Banks don’t want to offer overdrafts to cover cashflow gaps, and big business doesn’t want to pay invoices quickly. That creates a problem which needs a solution.” MarketInvoice, of course, being the solution: monetizing an invoice that hasn’t been paid yet by applying new technology to an old financial product — factoring. Stocker is adamant that “our service isn’t used for damage control,” which one might assume when a company seeks cash on an unpaid invoice, but instead “a pro-active boost for entrepreneurs set on rapid growth and expansion”. Clients use the service an average of 14 times in the first year, so that rather than some sort of glorified pay-day lender, “we’re a consistent financial partner”.

Both MarketInvoice and Funding Circle are partnered with the British Business Bank, an arm of the UK government, which represents further evidence of the industry’s evolution: state acceptance. In September the bank increased the level of government support into MarketInvoice to £10m, with the original £5m having already facilitated over £50m worth of funding to small businesses across the UK, according to Stocker.

“Government money is efficiently channelled through an agile funding platform that’s accessible to all business owners,” he says. “At the same time that money is earning a healthy return. It’s a win-win for everyone involved.”

Banks want a piece

“Referring business to us allows banks to keep their customer rather than just turning them down for a loan,” says Natasha Jones, communications manager at Funding Circle. “They can maintain that relationship.” RBS also refers business to Funding Circle.

“I think it’s highly likely we’ll start to see the banks simply embrace their new rivals, partnering with leading fintech companies,” says Stocker at MarketInvoice. “In asset classes such as invoice finance and equity funding, it’s clear the traditional institutions are being left behind.”

Today, it seems barely a week goes by without the mainstream teaming up with the young upstarts. In late November, Standard Life said it was in discussions to provide product for Chinese P2P firms’ online platforms, though there were challenges around satisfying know-your-client requirements.

China is no stranger to P2P — two established businesses, active both onshore and offshore, are Credit China and CreditEase — and the approach also fits very well with the risk-sharing principles of Islamic finance. In Malaysia alone, Shariah crowdfunding platforms include Make the Pitch, myStartr, pitchIN and Social Sharity, while equivalents also exist from Pakistan (Seedout) to the UAE (Eureeca and Aflamnah), Indonesia (Bursalde and Wujudkan) to Egypt (Shekra and Yomken). HalalSky is an example of a Shariah-themed crowdfunder launched in the US, and for that matter, CrowdCube has been certified as Shariah-compliant in the UK.

Another interesting step was Funding Circle acquiring the German marketplace lender Zencap in October, giving it a presence in Germany, Spain and the Netherlands to add to its US and UK operations. There is a temptation, therefore, to think of crowdfunding as becoming a cross-border phenomenon, though that may be premature. “At the moment, we are regulated in each geography so there are restrictions around what we can do at the moment,” says Jones.

That said, on November 25 Funding Circle launched a £150m listed vehicle on the London Stock Exchange, the proceeds of which can be lent in any geography the company enters. “That will be a way for investors to access global SME fixed income,” says Patel, who says it is the first time it has been done by any platform.

And P2P operators are not the only ones to see a gap. BlueBay Asset Management, for example, has run a private debt strategy since 2011, lending money directly to European high yield companies. Its Direct Lending Fund held a financial close in 2013 after raising €800m of commitments from institutional investors.

Bubble trouble?

Naturally, he believes practices at Funding Circle, with a sophisticated analysis of credit and risk, are strong, and actually welcomes the prospect of a crisis of sorts, believing it will allow people to differentiate between businesses that understand credit and those that don’t. Jones says she “worries about a platform going down and the reputational risk that poses, especially when larger platforms in the UK and US have worked so hard to build up consumer confidence.”

Seeing this concern, some institutions have tried to get ahead of the problem by opening their books. Landbay, a British P2P lender which prides itself on having published full details of its loan book, commissioned an independent analyst, MIAC, to put it through the same stress testing that any UK bank would be required to go through by the Bank of England, then published the results.

It says the outcome was an average expected loss rate of 0.03% before interest payments based on the BoE’s base case, and 0.48% under the BoE’s stress test scenario (GDP down 3.5%, unemployment rising to 9% and UK house prices falling by 20%).

Every lending platform publishes default expectations, but the truth is it’s a little early to tell what they’re likely to be. An attempt was made by the research group AltFi to provide some definitive data around losses after Tracey McDermott, the acting chief executive officer of the FCA, was asked by the Treasury Select Committee if she could provide a number representing the level of losses suffered by investors in UK equity crowdfunding to date, and was unable to do so.

AltFi studied the 367 companies that had crowdfunded at the five largest UK equity crowdfunding platforms from 2011 to June 2015. It found that over 80% of the companies funded between 2011 and 2013 were still trading, a result it describes as “impressive” given that 55% of UK SMEs don’t survive five years (according to a 2014 study by insurer RSA).

Looking at the 2013 generation as an example, 22% had gone on to raise further funds at a higher valuation or had realised a return for investors via a successful exit, while 28% had either failed or were showing signs of difficulty. The study measured the portfolio return of the industry since inception, measured as an IRR, at just 2.17%, but the picture changes completely if relevant tax reliefs (in the UK, SEIS and EIS) are fully used, bringing that return to 33.79%.

Some see no reason for concern. “People talk about the alternative finance bubble, forecasting an inevitable peak before it all comes crashing down,” says Stocker. “We believe the sector shows no signs of slowing down. Yes, some of these businesses will fail — the same is true in any industry. The market has become saturated with new providers and only the best of these will survive.” He says partnerships, acquisitions and mergers lie ahead.

It’s certainly true to say that the industry still has headroom. Ian McAfferty, Monetary Policy Committee member at the Bank of England, addressed the subject in a speech in October. “It is important to stress that this type [P2P] of external finance is still small compared to bank lending, on which SMEs remain heavily reliant,” he said. “In the first half of 2015, for example, P2P lending to SMEs was less than 20% of the flow of net bank lending to SMEs.”

But it’s only just got started. “Alternative finance is growing,” McAfferty said, “and is likely to be a developing feature of the market in future years.”