Latest news

Latest news

◆ Fast money reverses out of SSA bond market ◆ CLO managers face risky ramp startegy ◆ Corporate hybrid bond market runs hot despite volatility

Manager tightens spread on triple-A rated notes by 23.5bp compared with the original deal

Lower loan prices offer higher equity returns but managers face rally risk once deals are priced

More articles

More articles

-

Neuberger Berman has hit the market with its first collateralized loan obligation since the crisis.

-

JPMorgan, Barclays and Bank of America Merrill Lynch continue to dominate the top three bookrunning slots, respectively, in global asset-backed securities this year, according league tables provided to SI by Dealogic.

-

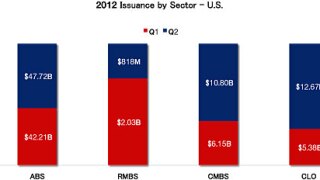

The securitization market continued to gain speed in the second quarter of 2012, surpassing the first quarter as the strongest overall for the market since the financial crisis.

The securitization market continued to gain speed in the second quarter of 2012, surpassing the first quarter as the strongest overall for the market since the financial crisis. -

RBS collateralized loan obligation analyst Justin Pauley gave notice to the bank that he plans to leave his post for a buyside position at Brigade Capital Management, a New York City-based hedge fund.

-

Ratings of Spanish small and medium-size enterprise collateralized loan obligations remain resilient even if collateral performance deteriorate significantly as long as sovereign and counterparty risk does not increase, according to Fitch Ratings.

-

Greg Stoeckle, managing director and Head of Global Bank Loans at Invesco, which last completed a $350 million dollar deal in April (SI, 3/24), spoke with managing editor Graham Bippart about what’s driving issuers into the market, how the market is evolving and what’s in store for the sector.

-

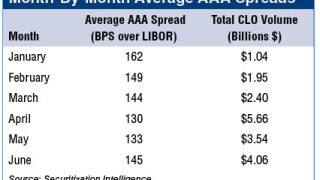

Three collateralized loan obligations totaling nearly $1.5 billion were priced by early Thursday afternoon this week, even as spreads on liabilities drifted wider to levels similar to those seen in February this year, when AAA-rated liabilities were consistently being priced in the area of 150 basis points, according to SI data.

-

Around a dozen new-issue collateralized loan obligations are set to come to market ahead of the traditional summer lull.

-

U.S. commercial mortgage-backed securities and collateralized loan obligations have performed better than expected, while residential mortgage-backed securities and real estate collateralized debt obligations have been the worst performing among all structured finance sectors, according to Fitch Ratings.