Although volatility in the fixed income markets and a decline in liquidity all trickled down to the broader ABS market, fear of the unknown was the key factor in the poor performance of Federal Family Education Loan Program (FFELP) and private student loan ABS last year.

Many blamed the rating agencies, with investor concerns over the threat of widespread downgrades of FFELP ABS from Moody’s and Fitch triggering a sell-off which caused spreads on existing FFELP paper to widen.

According to a report issued by Fitch last November, the reasons for the proposed changes stem from a slowdown in payment rates that placed existing FFELP ABS at higher risk of missing stated maturity dates. Moody’s closed the comment period for its proposed changes on October 30, and declined to comment on its outlook for 2016.

Additionally, the US Department of Education announced policy changes in the fourth quarter that further fueled investor fears. This included the expansion of income-based repayment to more borrowers. Under the Revised Pay As You Earn (REPAYE) Plan, which kicked off in December 2015, any Direct Loan (FDLP) borrower can cap their monthly payments at 10% of discretionary income and have any remaining undergraduate debt forgiven after 20 years. This softened the previous income based repayment rule, wherein monthly payments had a floor of 15% of discretionary income and debt was forgiven after 25 years.

“An increasing number of borrowers opting into the Pay As You Go and REPAYE programmes would have the effect of reducing current payments and extending out the terms of the loans,” explains Richard Fried, of counsel at Stroock & Stroock & Lavan in New York. “[The rating agencies’] concern is that under extreme stress scenarios, some of the earlier maturing tranches of outstanding FFELP securitizations may not be paid in full by their legal maturity date.

In a comment letter to Moody’s regarding proposed changes to its ratings methodology last summer, Navient, the US’s largest students loans company, wrote: “We agree with Moody’s that there have been some periods in the recent past in which repayment activity was at levels below historical norms, [but] we believe that Moody’s proposed methodology reflects a disproportionate response to the overall degree of extension risk in pools of FFELP loans.”

Following in Moody’ footsteps, Fitch Ratings also proposed amendments to its rating criteria for FFELP ABS on November 18. Fitch accepted feedback on the proposals during the consultation period, which ended on December 31, 2015.

Michael Dean, a managing director at Fitch, mentioned that during the exposure period, bonds that potentially faced downgrades would be placed on watch. “Following formal adoption of the criteria, we would expect to take rating actions on any affected bonds over a six month period,” he says.

Some investors felt that fears over the rating agencies’ decision to make changes to their methodologies were overblown. “It does make an impact, it’s not immaterial,” says Ron D’Vari, chief executive at NewOak Capital, an ABS advisory firm in New York. “[But] just because you change the ratings doesn’t mean that the cashflow changes on the portfolio”. D’Vari also notes that the change will likely put a damper on new issuance.

Domino effect

The ratings agencies’ move to change their FFELP methodology also hit the private student loan market. When FFELP spreads widened, spreads on private student loans also widened out in sympathy. “This is an example of herd mentality — when investors get scared they shy away from the entire sector,” says Fried.

This view is echoed by Theresa O’Neill, managing director at Bank of America Securities, who also emphasises that headline risk factored into poor student loan ABS performance last year.

“[Even with] federal regulators like the Consumer Financial Protection Bureau (CFPB) starting to make a distinction between the federal and private student loans, it’s still under a big umbrella of student loans,” she says. “But sometimes something totally unrelated to the private student loan sector gets picked up by the media… so that constant headline risk has also weighed down on the market.”

Silver lining?

Although uncertainty remains as to what changes Moody’s and Fitch will make to their FFELP ratings methodology, some buying opportunities have arisen as spreads have widened.

“We do think triple-A safe FFELP ABS… that pass Moody’s proposed triple-A scenarios, offer good value and should see spreads recover faster after all the rating actions are said and done,” wrote JP Morgan analysts in a research note in November 2015.

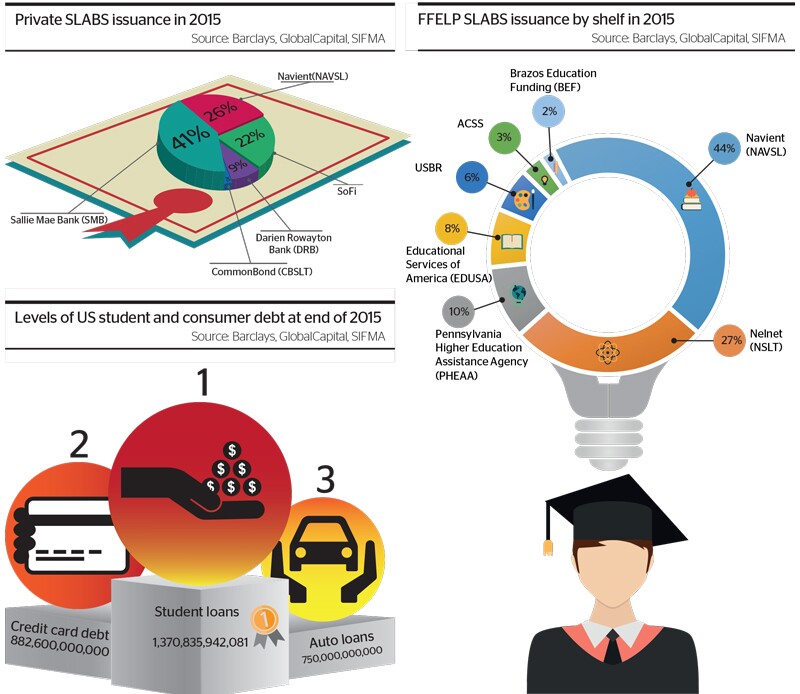

Similarly, despite the decline in SLABS issuance for a third consecutive year, ABS analysts at Barclays maintain a “positive view” on both FFELP and private student loan ABS going into this year. Issuance in 2015 reached $11.5bn through mid-November, as compared to $15bn and $19bn in 2014 and 2013 respectively.

Fried points out that performance of the private student loan sector in 2016 could boil down to the decision to securitize by big issuers in the industry.

“If Sallie Mae, Navient etc decide to do a few securitizations that is going to drive the market significantly. If they sit on the sidelines that’s going to have a negative impact,” he says. “SoFi, CommonBond and a few other smaller issuers are going to do a few deals but that alone is not going to drive the market much.”

Bank of America Securities’ O’Neill, on the other hand, says that relative value decision would potentially define SLABS performance this year. “People [will] look at the relative value… I have one product that’s widening out and another product without these structural problems, but the FFELP ABS are cheaper [so] that’s what I’m going to buy.”