The global financial crisis damaged more than just the economy — it left an enormous swathe of the US population without access to conventional forms of credit. One lasting legacy of the crisis has been the portrait of the irresponsible subprime borrower, and the image has stuck with banks and regulators, which have both made efforts to reign in lending to this segment of consumers.

“There is a stigma now. Many people think that subprime consumers take payday loans because they don’t know any better. It’s not because of that,” says Krishna Gopinathan, chief executive of Applied Data Finance, referring to short-term loans with high interest rates. “They just don’t have any other opportunities. It’s easy to make assumptions when you don’t meet these consumers and just jump to conclusions that aren’t really accurate.”

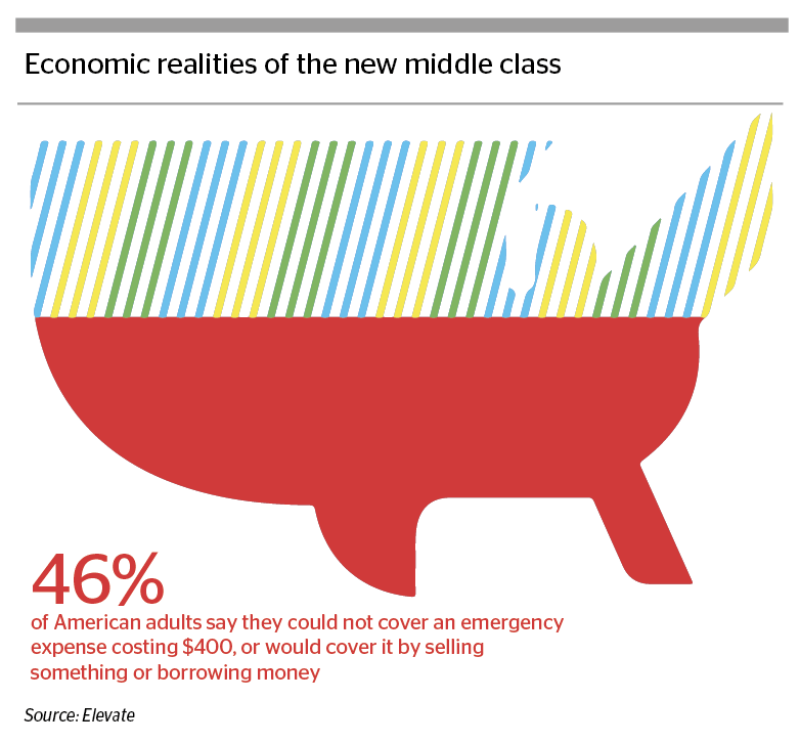

According to a report put out at the end of 2016 by the Centre for the New Middle Class, a research group at subprime lender Elevate, a ‘subprime’ status can have financial consequences, with these borrowers being six times more likely to have been denied a job in the prior 12 months because of low credit. They are also nine times more likely to have been turned down for credit in the prior 12 months, and 10 times more likely to say they could not “make financial progress” because of low credit.

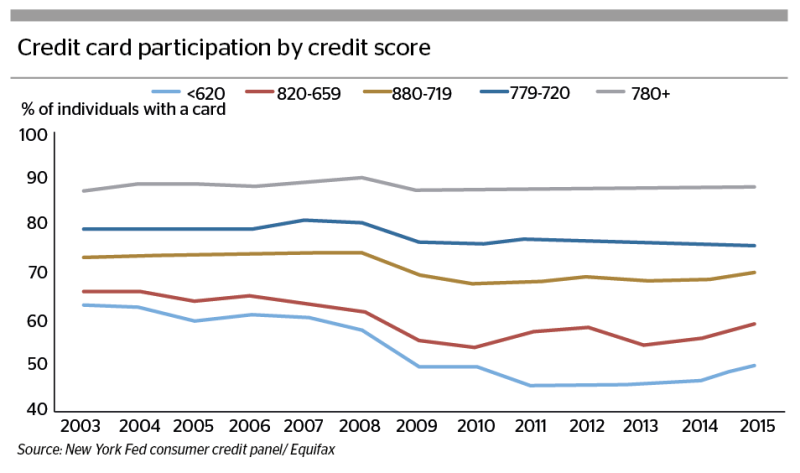

In securitization, the pullback in subprime consumer lending — especially for non-auto related sectors — has also been deeply felt, with subprime consumer ABS issuance slowing to a trickle in the post-crisis years. For the five major credit card issuers, 2008-2016 saw revolving credit available to US borrowers with a FICO score of less than 660 — regarded as the threshold for subprime status — reduced by approximately $142bn, according to data provided by Elevate.

“Subprime borrowers are the only group whose balances haven’t yet caught up with the peak they reached in 2008,” says Joelle Scally, an administrator at the Centre for Microeconomic Data at the New York Federal Reserve. “Everyone else is pretty close to that 2008 peak, but subprime borrowers are 6% below that. Their balances have really shifted in composition — they’re made up of more auto and student loan balances, because it’s very difficult for subprime borrowers to get mortgages or credit cards right now.”

The majority of lenders’ efforts are heavily directed at prime and so-called ‘super-prime’ borrowers, which form a declining percentage of US consumers. Even online marketplace lending — an industry which emerged in the wake of the recession and which many thought would fill the bank void — mostly targets borrowers in the ‘near-prime’ range of 640-680.

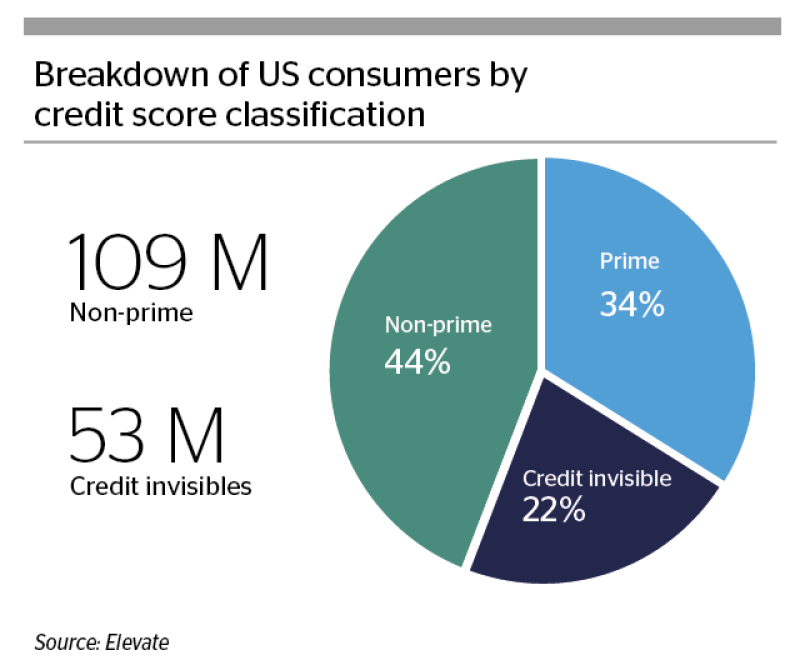

“There’s more subprime consumers now — by our calculations, two-thirds of the US either have a credit score below 700, or no credit score at all, yet there is less and less credit available to them than ever before,” says Ken Rees, CEO atElevate.

Don’t judge a book by its number

With a huge portion of the US underserved by traditional lenders, some observers believe that the solution to widening access to credit hinges on looking beyond credit scores, which follow borrowers like a ball and chain.

“We’ve all gone through things in our lives that have had a financial impact on our credit scores, whether it’s a medical situation or a divorce. It gets recorded at the credit bureaus as a black mark, and because of that long memory the credit bureaus have, there’s an innate, backward-looking impact,” says Gopinathan. “It makes the assumption that what you were in the past is what you’ll be in the future.”

Rees also highlights that some lenders tend to overlook the nuances between underwriting to secured credit products versus the customer.

“The problem with subprime mortgage and auto paper is that they’re secured credit. Oftentimes lenders are making loans predicated on the collateral and not the customer. Lenders aren’t really looking at things like ability to repay, or underwriting to an individual and that’s where you get the problems,” Rees says. “If you’re not underwriting correctly, that’s a problem,” he warns.

Meanwhile, some credit reporting companies are incorporating the predictive power of machine learning into newer versions of credit models, hoping to improve the ability of lenders to underwrite borrowers with little or no credit history.

VantageScore Solutions has announced the incorporation of machine learning into its latest credit score model, which is on track to be rolled out later this year.

“Machine learning techniques — because they’re sort of power platform dynamics — when you process lots of different scenarios hundreds and thousands of times, they’re able to come up with insights and connections in the data that we normally wouldn’t be able to find,” says Sarah Davies, senior vice president of analytics at VantageScore.

“When we look at collections information on the credit file — that’s very predictive of people who’ve historically gone bad or could likely go bad again. What the machine learning techniques did was to link collections information with the enquiries information, which created a variable that was very predictive of people who don’t have that much information,” Davies adds, noting that the new model gave a 30% improvement in scoring accuracy among consumers with little available credit data.

Securitization’s potential

In a twist on the subprime mortgage crisis, securitization may be key to opening up more funding for what some people call “credit invisible” borrowers.

While the market for subprime consumer ABS dried up in the years after 2008, the past 18 months have seen a resurgence of deals backed by unsecured consumer debt. Apart from the auto sector, subprime consumer securitizations were not widely seen until the rise of online lenders such as Avant and Lending Club, which both target borrowers beneath the prime threshold. Avant, in particular, has become a regular issuer of unsecured subprime consumer loan ABS, and investors have piled into the bonds.

The Chicago-based marketplace lender priced its last transaction in April, having to increase the amount offered and tightening all classes of the capital structure. Borrowers in that deal had an average FICO score of 655, according to pre-sale information from Kroll Bond Rating Agency. Investors have been drawn to the bonds for their short duration and relative high yields. Avant’s offering was priced at 115bp over the euro dollar spot forward for its senior single-A rated tranche. The bonds have a duration of 0.5 years.

Regulators take note

Consumer finance observers also point out that the burden that subprime consumers face is not just aggravated by banks getting out, but also in part by a misreading of the crisis by some regulatory agencies.

“What lenders choose to do is a function of what regulators have said, and how technology has evolved. So technology is moving on one path, regulators on another — lenders sit in the middle of the two and try to serve the customer,” Gopinathan says.

“I don’t think post-crisis legislation is harmful as opposed to how the Federal Deposit Insurance Corporation and the Office of the Comptroller of the Currency reacted to what happened during the recession,” says Rees. “We believe they misread the risk aspects of serving these consumers and overreacted to the real problem, which was essentially collateral fraud.”

He adds that banks want to

offer products to these customers, but have been told by examiners that they cannot make credit available to anyone with a credit score of less than 700.

Rees says that for lending conditions to improve, banking regulators need to help banks better serve subprime consumers, rather than cut off their access.

“You can’t always think that the answer to this problem is going to be a 12% installment loan or a credit card — there’s going to have to be a new breed of products and a new level of innovation that regulators should encourage in order to provide more responsible credit products for people who are right now stuck with payday loans, or pawn and title loans,” he says. s