-

Over recent years, hedge funds have widened the spectrum of their activities from hedging and trading on the derivatives and currency markets to building huge positions in credit markets by selling protection on credit derivatives, providing equity to the collateralized debt obligation market and investing in mezzanine tranches of subprime residential mortgage-backed securities.

-

Structured finance transactions, such as term securitizations, involve a variety of market participants, ranging from relatively small lenders and servicers to large financial institutions.

-

The second part of this Learning Curve covers quantitative modelling techniques and the assessment of model risk for constant proportion debt obligations.

The second part of this Learning Curve covers quantitative modelling techniques and the assessment of model risk for constant proportion debt obligations. -

Constant proportion debt obligations have gained a lot of attention in the structured credit market since their debut last summer.

-

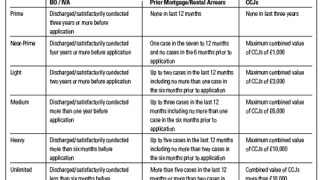

Over the last several years, a number of lenders have entered the specialized lender segment, focusing on subprime mortgages in the U.K.

-

In a market marked by strong credit performance and growing originations, it was accepted that 50 basis points was an adequate and profitable servicing fee.

-

This article will discuss privacy law issues arising in connection with the provision to asset-backed securities investors, or prospective investors, of nonpublic loan level information about the pooled assets underlying an ABS.

-

The pricing of bespoke synthetic collateralized debt obligation tranches has been described (accurately, in our view) as the "next biggest challenge since Black and Scholes invented their formula for option pricing."

-

Fitch Ratings looked at delinquency trends in the European residential mortgage-backed securities market by examining three-months plus arrears for each European country.