-

If Europe is serious about growth, it needs to get serious about securitisation. The PCS initiative should help.

-

A bit of movement on the syndicate front is always great news — and isn’t it amazing that these hires often take place in June so that movers can enjoy three months of summer?

-

If VTB manages, on its third attempt, to issue a sukuk then the Russian bank will have achieved for conventional issuers what Goldman Sachs couldn’t and Crédit Agricole didn’t dare. Demonstrating that such business is possible would do a big favour for the Islamic finance market — and the Russians themselves.

-

African deals have impressed with consistent oversubscriptions this quarter, but borrowers waiting on the sidelines must move quickly if they are to emulate others’ successes.

-

The successful sukuk issue by Dubai last week was an indication that its rehabilitation among investors is continuing well. But there were warning signs for other issuers too. Ignoring them would be foolish.

-

The market in Europe for commercial real estate finance has always been markedly different than that of the U.S.

-

Argentina's bullying tactics on YPF are not going to win it any friends, particularly in Spain. But with little foreign investment to be withdrawn and already low expectations among emerging market investors, the longer term impact is likely to be limited.

-

By John Bella, managing director and head of the commerical ABS group at Fitch Ratings, and Sean Egeran, director

By John Bella, managing director and head of the commerical ABS group at Fitch Ratings, and Sean Egeran, director -

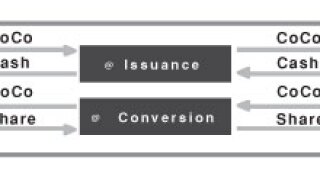

The bank regulatory capital consists of common stock, preferred stock, subordinated debt and hybrids, such as trust preferred and convertibles.