Latest news

Latest news

Spreads on CLO liabilities stay wide, making resets for deals from multiple vintages unattractive

Fund is designed to invest in the equity in Bain’s CLOs, but can also invest in liabilities

Manager trims spreads on CLO’s investment grade tranches in partial refinancing

More articles

More articles

-

A secondary option for risk retention in collateralised loan obligations, proposed by the FDIC in the final version of the Dodd-Frank rules on Tuesday, has been dismissed as “completely unworkable” by a senior executive at the Loan Syndications and Trading Association.

A secondary option for risk retention in collateralised loan obligations, proposed by the FDIC in the final version of the Dodd-Frank rules on Tuesday, has been dismissed as “completely unworkable” by a senior executive at the Loan Syndications and Trading Association. -

Continued spread pressure in the US CLO market has forced managers completing deals in the past two weeks or so to swallow higher spreads to get their deals over the line, with many hoping they can take advantage of softness in the underlying leveraged loan market to make up for the wider print.

-

American Capital, which earlier this year brought one of the first US collateralised loan obligations to comply with European risk retention rules, is aiming to replicate the success of that deal with a new CLO it announced this week.

-

Nomura’s head of leveraged credit sales has left the bank’s New York office.

-

The eternal tussle between equity and triple-A investors in collateralised loan obligations intensified this week, as a widening in triple-A CLO spreads drove down equity returns even further and forced some arrangers and managers to make concessions in order to lock senior debt investors into their deals.

-

The bull market in US collateralised loan obligations showed signs of running out of steam this week. With a huge amount of supply still in the pipeline as managers try to ramp up assets under management before risk retention rules are finalised, some deals in the market are having trouble getting over the finish line after a torrid time for secondary triple-A and double-A spreads last week.

-

Onex Credit Partners, the collateralised loan obligation manager arm of Canada’s Onex Corporation, is making a push into the expanding European CLO market with a new hire, the firm announced today. The move comes amid a growing trend of US managers trying to access European investors.

-

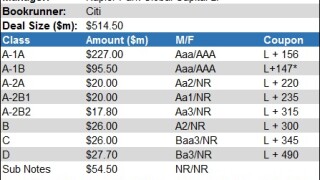

Napier Park Global Capital has priced the fifth collateralised loan obligation in its Regatta series, with the significantly wider pricing levels of the triple-A tranche showing the effect of poor secondary liquidity in senior CLO paper on primary supply.

-

Japanese investors are helping CLO managers price their deals as the end of the year approaches, filling a gap left by US triple-A investors that don’t have room left for new deals. Amid widening triple-A spreads and secondary market volatility, equity returns are suffering — but widening spreads in the underlying leveraged loan market may help offset that decline.